Inflation and the “Post-Pandemic” Portfolio

Just as we have adjusted to everyday life with a global virus, and worked through waves of Delta, Omicron and BA2, BA4, BA5, our financial lives are beset with old fears about inflation, recession and financial market declines. We knew that we would not be able to just flip a switch and turn the post-pandemic economy back up to full speed, but the shock of inflation spikes, shortages and grim stock market news is nonetheless difficult to bear. How can you best manage your money as we move (eventually) out of the pandemic?

The core components of a portfolio are cash, bonds and stocks. Each play a role, and by diversifying (holding a little of each), typically there is always something “working” in your portfolio, something that is growing, or at least holding steady. (Diversification also means there is always some part of your portfolio NOT working so well.) Each component responds to market forces (interest rates, inflation, geopolitical events) differently. Over the past three quarters, all have been challenged. Let’s take a look at each in turn, and then on strategies to adapt.

STOCKS

Stocks are the growth engine in any portfolio. The larger the company, the greater likelihood it produces growth in your portfolio by sharing its profits through dividends. Newer, smaller companies offer a pure growth strategy: you invest because they offer a product or service that is likely to become dominant, and as the company’s implementation of its plans grows, so does its stock price, and that stock price appreciation grows your portfolio.

The US economy, like the rest of the developed world, is a consumer economy. Countries measure their economic activity in terms of their Gross Domestic Product (GDP). In the US about 70% of our GDP was from consumer spending. That’s you and me going to the grocery store and Target. The rest of US GDP was from private investment (19%), meaning making stuff rather than buying it (constructing commercial

This a long way of explaining that if we don’t have money to spend, economic growth can stall. Neither the private sector nor the government are going to make up the difference.

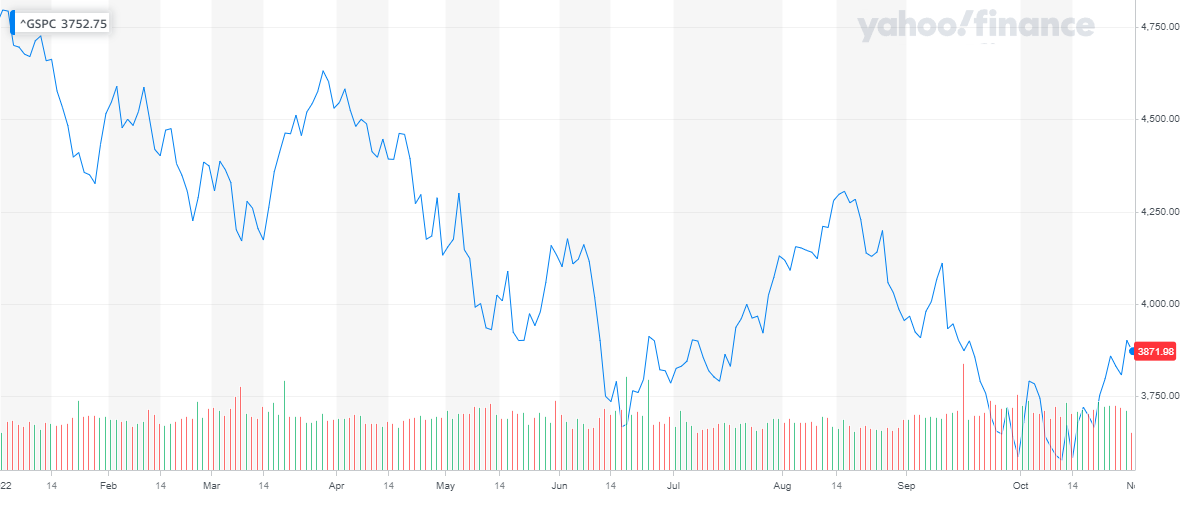

As we ended last summer, with the economy continuing to open, supply chain weaknesses created shortages of goods and inflation started to creep up. Remember the Even Given? The gigantic boat that blocked the Suez Canal? That was last March. As we ended the year, the debate about whether inflation was transitory heated up and stock prices started to wobble.

Fast forward to this year. At the end of February, Russia invaded Ukraine and now major inputs into the global economy were affected: energy and other commodities like wheat. If you cut off supply of something, and if demand remains the same, prices will increase provided consumers can pay higher prices and no price controls are implemented by government. The idea that democracy could be at risk worldwide did not sit well with financial markets, either.

We have forgotten this now, but the stock market surged in March, only to drop dramatically towards the end of the quarter. Then stocks came roaring back, only to decline in fits and starts through April and May, then made a modest comeback mid-summer. The Fed raised rates 0.25% in March, by 0.50% in May, and by 0.75% each time in June, July and September. The Fed meets this week and bets are for another rate hike.

One of the weird things happening in financials at mid-year was that sectors that typically are interest rate-sensitive, like real estate, had not shown signs of being tapped out. And so the bumps upward continued.

There is a lot of talk about how the Federal Reserve should have known better and adjusted faster to upticks in inflation last Fall. It’s not the Fed’s job, however, to forecast political events, and it’s not reasonable to believe that they should have foreseen the invasion of Ukraine, the strength of the Ukrainian people to fight back, or the global response to the attack on a sovereign nation.

There are also other forces at work that make financial forecasting especially challenging, including:

- The move by OPEC+ to restrict oil production, keeping prices high;

- Russia’s continued assault on Ukraine and its recent reversal on the Black Sea grain deal, threatening Ukraine with widespread starvation and wreaking havoc with commodity prices;

- China’s on-again-off-again lockdown and the repercussions on the global economy;

- US companies’ willingness to restrict production to increase prices and profits (airlines), and to reap record-breaking profits from price increases (oil, retail).

BONDS

Bonds (the money you lend to someone else – to a company through corporate bonds, to governments through its debt (like US Treasuries issued by the federal government and municipal bonds issued by state and local governments), and to individuals (through things like mortgages) complement stocks by not relying on the sale of products or services, but on the credit quality of the borrower.

One of the reasons US Treasuries are considered a “safe haven” in times of financial turmoil is because all things being equal, we’re pretty sure the US government will pay its debts.

Yet bonds aren’t risk-free. In addition to the possibility of default by the borrower, there is also the impact of changes in interest rates and inflation. The interest rate on a bond contains both a reward to the lender by way of the interest the borrower pays, and an inflation component, since tomorrow’s money won’t be worth the same as that money today. As interest rates and inflation rise, the price of existing bonds falls. That $10,000 you loaned out yesterday at 5% could be loaned out at 6% today, and so the price of yesterday’s loan (i.e. the bond you’re already holding) falls. This decline in value, though, is on paper: if you hold onto that old bond, you’ll be repaid what you expected, plus have your principal (the amount you lent) returned. Provided the borrower does not default.

With both inflation and stock prices, it is also important to remember that recent high stock prices have been based on maneuvers like stock buybacks and pent-up demand due to two years’ of the pandemic. Price levels have jumped dramatically following an extended period of very low inflation, and even talk of deflation. The whipsaw turnaround is bound to feel worse than if it had happened more gradually over a longer period.

CASH

When everything else is going to Heck – stock prices falling, rising inflation, prospect of job loss, maybe recession – Cash is King. Yet holding cash is almost always a losing proposition: it will almost never keep up with inflation. AND YET I will always advise you to have some on hand: for the unexpected (your Emergency Fund) as well as for investment when opportunities present themselves.

Everyone hates holding cash until they need it.

We all want to be living in a “post-pandemic” world. We are done with surprises, and we just want things to get back to normal. The universe, however, has a different idea. Regardless of what we might want, 2022 so far has been anything but a smooth ride out of Corona Times. If you’re looking at facts, we have not, in fact, left the pandemic behind.

WHAT TO DO

- Shore up cash reserves. Replenish your Emergency Fund.

- If you are working and considering a move, lock in your new job.

- If you are retired or close to retirement, lock in your next couple years of sources of income to pay expenses. Keep at least 12 months of expenses in cash, and the next couple of years or more close at hand – CDs and short-term bonds. Keeping saving in the stock market means exposing it to further volatility.

- Look to pay down/ pay off any variable rate debt (HELOC, credit cards, student loans). One place where inflation can work in your favor is with fixed rate debt but variable rate debt will cost you more as time goes by.

- If you’re in the market for a house, review the cost-benefit of renting v buying, and remember home purchases are long-term decisions. Also remember that is you have to move, you have to move, and rates won’t necessarily stay high forever.

- Review your expenses and divide into Non-Discretionary (Housing, Food, Insurance) and Discretionary (Travel, Entertainment, Retail Therapy)

- Review your goals and check on whether your resources are aligned.

- Rebalance as indicated

- As the prospect of Winter approaches, review your exercise program. One of your biggest assets is your good health – physical, mental and emotional. Make sure you are tending to it.

Lastly, and in case you have been battling FOMO over teenagers making major money in Bitcoin and NFTs, those markets have had a major throttling this year, too.

One of the hardest parts of planning is sticking with the plan. The reason you have it is to help you negotiate times like these. No time like the present to use it.